VAT in African trade: A guide for global e-commerce brands

TL;DR:

- Most international brands overlook VAT’s operational role in African trade, risking costly mistakes. Proper understanding and compliance with VAT mechanisms, classifications, and digitalization are crucial for efficient cross-border export and import processes. Building robust VAT workflows and leveraging specialized platforms like MoreShores can turn VAT management into a competitive advantage.

Most international brands entering African markets treat VAT as an afterthought, something to sort out after the logistics are running. That assumption is expensive. The role of VAT in African trade is far more operationally significant than a line item on a customs declaration. From export zero-rating documentation to destination-based tax allocation under the African Continental Free Trade Area (AfCFTA), VAT shapes your pricing, cash flow, audit exposure, and your ability to clear goods efficiently. This guide breaks down what you actually need to know before your first shipment clears customs.

Table of Contents

- How VAT works across African countries and its impact on trade

- VAT zero-rating versus exemption: Key distinctions for exports

- Challenges and reforms in West African VAT systems affecting trade

- The AfCFTA destination principle and VAT allocation in African trade

- Practical steps for e-commerce and logistics teams to manage VAT compliance in Africa

- Why relying on simplified VAT export assumptions can threaten your African expansion

- How MoreShores supports your VAT compliance and cross-border trade in Africa

- Frequently asked questions

How VAT works across African countries and its impact on trade

Value-Added Tax (VAT) is an indirect consumption tax charged at each stage of the supply chain on taxable supplies of goods and services, as well as on imports. Unlike a simple sales tax applied once at the point of sale, VAT is collected incrementally. Each business in the chain charges output VAT on what it sells, then deducts input VAT it paid on its own purchases. The difference is what gets remitted to the tax authority.

This non-cumulative design matters for cross-border trade. It prevents “tax cascading,” where a product is taxed multiple times on its full value at each transaction stage. For e-commerce solutions moving goods across multiple African markets, this structure means VAT costs can be recovered, provided your compliance records are in order.

Here is how VAT flows in a standard African import scenario:

- A foreign brand ships goods into South Africa. VAT is charged at the port of entry on the customs value of the goods.

- The South African importer pays that import VAT, which becomes input VAT claimable against output VAT on domestic sales.

- The end customer pays VAT embedded in the retail price. The retailer remits net VAT (output minus input) to the South African Revenue Service (SARS).

- If a vendor’s input VAT exceeds output VAT in a period, a refund is owed by the tax authority.

The practical impact on trade is significant. VAT on imports creates an upfront cash cost that only recovers over time through the refund mechanism. For brands shipping large volumes into markets like Nigeria, Kenya, or South Africa, miscalculating this timing affects working capital. Understanding what is VAT in African trade, not just the rate but the mechanics, is the first step to building a cash flow model that actually holds.

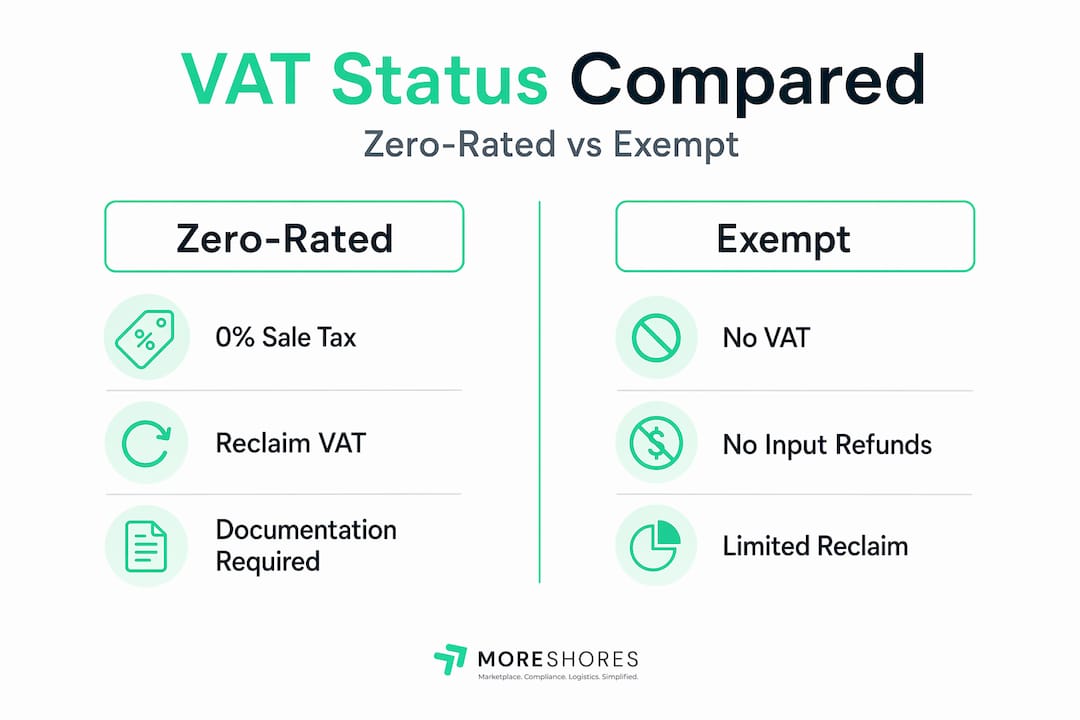

VAT zero-rating versus exemption: Key distinctions for exports

This is where many international brands make costly mistakes. Zero-rating and exemption sound similar but they have opposite effects on your cost base.

When goods are zero-rated, VAT is charged at 0% on the sale, but the seller can still recover input VAT paid on purchases related to that supply. For exporters, this is the favorable outcome. You do not charge your foreign customer VAT, and you get back the VAT you paid on your raw materials, packaging, or services used to produce those goods.

When goods are VAT-exempt, they fall outside the VAT system entirely. No VAT is charged on the sale, but the seller also cannot recover input VAT. The tax paid on inputs becomes a permanent cost embedded in your price. For high-volume cross-border trade, that embedded cost adds up quickly.

The key compliance distinctions for export scenarios:

- Zero-rating applies to direct exports where goods physically leave the country under customs control.

- For indirect exports, where a foreign purchaser or their agent collects goods locally, registration and documentation requirements are stricter. The purchaser must be registered as an exporter, and their details must appear on the SAD 500 (Single Administrative Document) customs form.

- SARS auditors specifically check whether the entity named on the SAD 500 matches the registered exporter. A mismatch triggers disputes and disallowed zero-rating claims.

- Misclassifying a zero-rated export as exempt, or vice versa, creates either an underpayment risk or an unnecessary cost burden.

Pro Tip: When setting up trade compliance processes for African exports, build a documentation checklist that includes SAD 500 verification as a mandatory step before every indirect export shipment, not a retrospective audit exercise.

The VAT implications for African commerce run deeper than most logistics managers expect. Getting this classification right before you go live saves significant time in audit defense later.

Challenges and reforms in West African VAT systems affecting trade

West Africa represents one of the fastest-growing consumer markets on the continent. It also represents some of the most fragmented VAT environments you will encounter. Nigeria, Ghana, Senegal, Côte d’Ivoire, and their neighbors each operate distinct VAT regimes with different rates, exemptions, filing frequencies, and digital infrastructure maturity levels.

The result is a compliance environment that increases costs and disrupts trade for any brand operating across multiple West African markets simultaneously. You are not dealing with one system. You are dealing with fifteen.

Five key challenges and reform developments you need to track:

- Inconsistent VAT rates. Standard rates range from 7.5% in Nigeria to 18% in Uganda, and exemption categories differ widely. A product zero-rated in one country may be fully taxable next door.

- Lack of digital infrastructure. Many West African tax authorities still rely on manual filing systems, which creates delays, errors, and audit exposure for brands with high transaction volumes.

- WATAF’s digitalization push. The West Africa Tax Administration Forum is calling for e-invoicing and automated filing systems across member states to reduce revenue leakage and lower compliance costs.

- ECOWAS VAT Directive adoption. The Economic Community of West African States has issued a VAT Directive aimed at harmonizing tax regimes across the region, creating a more unified market for cross-border trade.

- January 2027 deadline. Member states are expected to domesticate the ECOWAS VAT Directive into national law by January 2027. Delays in alignment risk undermining investor confidence and stalling cross-border business activity.

“Aligning national VAT frameworks with the ECOWAS Directive is not optional for sustained economic integration. The 2027 deadline is a turning point for West African commerce.” Business and Financial Times Editorial, April 2026

Pro Tip: If you are planning West African market entry in 2026 or 2027, build your marketplace integration solutions and compliance workflows with the assumption that VAT rules will change during your launch window. Design for adaptability, not just current-state compliance.

The AfCFTA destination principle and VAT allocation in African trade

The AfCFTA is reshaping trade policy across 54 African nations. Its tax framework applies the destination principle to VAT, meaning VAT is imposed where consumption occurs, not where the goods originate. For international e-commerce brands, this has direct operational implications.

| Scenario | Origin principle | Destination principle (AfCFTA) |

|---|---|---|

| VAT charged where | Goods are produced | Goods are consumed |

| Risk for cross-border trade | Double taxation | Local VAT registration may be required |

| Pricing implication | Seller’s home VAT rate applies | Buyer’s country VAT rate applies |

| Invoicing requirement | Origin country VAT number | Destination country compliance |

| Export treatment | Taxed at origin | Zero-rated at origin, taxed on arrival |

What this means for your operations:

- Your export invoicing must reflect zero-rating at origin and account for the destination country’s VAT treatment on arrival.

- If you cross revenue thresholds in a destination country, cross-border invoicing must include local VAT registration numbers and compliant tax identification.

- Pricing models for African markets cannot simply apply your home country VAT rate. You must model destination-country VAT into landed cost calculations.

- The destination principle eliminates double taxation risk when applied correctly, which supports competitive pricing in destination markets.

- Aligning your customs and tax processes toward the destination country enables faster clearance and fewer disputes at the border.

The VAT compliance solutions you need for AfCFTA-era trade are destination-oriented from the start. This is not a future consideration. It is the current operating reality for brands trading across African borders today.

Practical steps for e-commerce and logistics teams to manage VAT compliance in Africa

Knowing the rules is not the same as having a compliance workflow that actually executes them. Here is a practical framework for e-commerce and logistics teams.

VAT registration and documentation checklist:

- Register for VAT in every country where you meet the registration threshold or are required as an importer.

- Verify that your entity is correctly registered as an exporter for any indirect export transactions.

- Ensure your details, not your freight forwarder’s, appear on SAD 500 forms for relevant shipments.

- Maintain copies of all export documentation for a minimum of five years to support audit defense.

- Issue VAT-compliant invoices that include your VAT number, the customer’s VAT number (where applicable), tax amount, and the supply date.

Step-by-step process for managing cross-border VAT submissions:

- Classify each product accurately under the relevant tariff code and determine the VAT treatment (standard-rated, zero-rated, or exempt) for the destination country.

- Set up compliance workflow optimization processes that flag high-risk transactions, such as indirect exports, for additional documentation review before shipment.

- Adopt digital VAT processing tools, including e-invoicing platforms and automated filing software, to reduce manual errors and support electronic audit trails.

- Reconcile VAT returns against your inventory and sales records monthly, not quarterly, to catch discrepancies early.

- Submit refund claims promptly when input VAT exceeds output VAT. Delayed claims create unnecessary cash flow pressure.

- Conduct an internal compliance audit every six months, focusing on export documentation accuracy and SAD 500 completeness.

| Compliance area | Common failure point | Recommended action |

|---|---|---|

| Export zero-rating | Incorrect exporter on SAD 500 | Pre-shipment document review |

| Input VAT recovery | Incomplete purchase records | Monthly reconciliation |

| Digital filing | Manual error in submissions | E-invoicing platform adoption |

| Multi-country registration | Missed thresholds | Threshold monitoring per market |

| Audit readiness | Fragmented records | Centralized document management |

VAT compliance risks rise sharply without procedural adherence to documentation and export regulations. And WATAF’s position is clear: standardized electronic evidence flows are the minimum expectation for compliant cross-border trade going forward.

Pro Tip: Treat your VAT compliance calendar the same way you treat your logistics schedule. Both require advance planning, real-time tracking, and accountability at each stage. A missed VAT filing deadline in a high-scrutiny market like South Africa or Nigeria carries the same operational risk as a missed shipment.

Why relying on simplified VAT export assumptions can threaten your African expansion

Here is a perspective most compliance guides will not give you directly: the biggest VAT risk for international brands in Africa is not the complexity of the tax code. It is overconfidence in how simple the rules sound on paper.

Zero-rating exports sounds straightforward. Ship the goods out, charge 0% VAT, reclaim your input tax. In practice, that sequence depends entirely on procedural and documentary adherence at every step, and exposure is tied to those specific details. An auditor does not care that your intent was to export. They care whether your entity name appears correctly on the SAD 500, whether your foreign purchaser was registered at the time of sale, and whether you can produce the original documentation on demand.

We have seen brands with genuinely compliant export intentions face disallowed zero-rating claims purely because their freight forwarder appeared on the customs form instead of the actual exporter. That is not a tax law failure. That is an operational process failure. The digital compliance insights that matter most are the ones that close that gap between knowing the rule and executing it correctly every time.

There is also a broader strategic point here. Without accelerated VAT digitalization and system harmonization, businesses face ongoing inefficiencies that block revenue and frustrate cross-border operations. Brands that invest in digital VAT infrastructure now, before regulators mandate it, gain a meaningful operational advantage over competitors still running manual processes. They clear faster, claim refunds sooner, and present cleaner audit trails. That is not just compliance. That is competitive positioning.

VAT challenges in African markets are real, but they are manageable. The brands that get into trouble are the ones that treat how VAT affects trade in Africa as a legal checkbox rather than an operational discipline integrated into logistics, IT, and finance.

How MoreShores supports your VAT compliance and cross-border trade in Africa

Navigating the VAT policies of African countries is genuinely complex, and building every compliance function in-house takes time your market entry timeline may not allow. MoreShores is built for exactly this challenge.

Our cross-border enablement services include acting as your Importer of Record, which means we handle VAT on imports, customs duties, and regulatory compliance directly, so your goods clear without delays tied to documentation gaps. Our platform supports electronic invoicing and audit-ready record-keeping across multiple African markets, from South Africa to Kenya to Nigeria. Through our e-commerce solutions, we integrate your product listings across Takealot, Amazon SA, Jumia, and Kilimall, with VAT-compliant invoicing built into the transaction flow. Our fulfillment and logistics operations maintain the export documentation standards, including SAD 500 accuracy, that protect your zero-rating claims. Partner with MoreShores to turn VAT compliance from a bottleneck into a structured, repeatable process.

Frequently asked questions

What is the difference between zero-rated and VAT-exempt goods in African trade?

Zero-rated supplies are taxed at 0% but allow full recovery of input VAT, while VAT-exempt goods fall outside the VAT system entirely and prevent input VAT recovery, making exemptions a hidden cost for exporters.

Why is VAT compliance more complex in West African countries?

West African VAT systems are fragmented across national lines with differing rates, exemptions, and digital maturity levels, making multi-country compliance expensive and disruptive until the ECOWAS harmonization deadline in January 2027 takes full effect.

How does the AfCFTA destination principle affect VAT in African cross-border trade?

Under AfCFTA, VAT is imposed where consumption occurs, meaning your pricing, invoicing, and compliance registration must be oriented toward the buyer’s country rather than where the goods were produced or shipped from.

What common pitfalls expose exporters to VAT audits in Africa?

The most frequent audit trigger is the SAD 500 form listing the wrong entity as exporter, particularly when a freight forwarder appears instead of the registered exporter, which leads SARS auditors to disallow zero-rating claims even when the export itself was genuine.